Under Armour Q4 Earnings Prep: Racing into the headwinds

UA reports Q4 and full-year fiscal 2026 tomorrow at 6:55 a.m. ET. Consensus is for revenue of about $1.17B (down ~1% YoY) and a loss of two cents per share. The stock trades around $6.43 against an average analyst price target of $7.73, with Truist, Barclays, and BofA all raising targets to $8 after the Q3 print and UBS the most aggressive at Buy with an $11 PT.

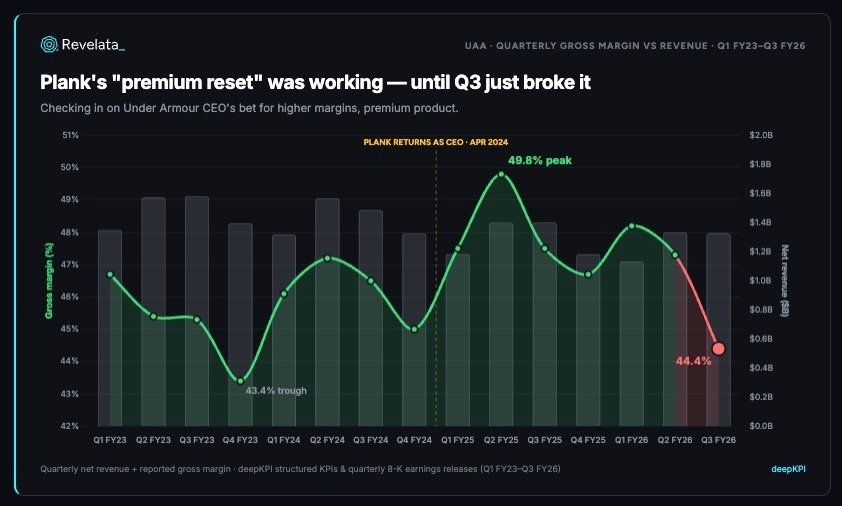

Kevin Plank returned as CEO in April 2024, five years after stepping aside, and immediately announced a turnaround predicated on moving upscale: shrink the top line on purpose in exchange for higher gross margins. This would involve exit wholesale, killing DTC discounting, selling MapMyFitness, separating the Curry Brand, and narrowing strategic focus to North America. To do this, he hired Eric Liedtke from Adidas to run brand and Yassine Saidi from PUMA to run product. The goal was to be smaller, but richer.

He’s not running it alone. Prem Watsa’s Fairfax Financial disclosed a 22.2% stake in early January, making Fairfax the largest shareholder. The position is roughly 42 million shares of non-voting Class A stock, which means Watsa has put chips on Plank without seeking governance influence. Plank’s also brought in a new CFO, Reza Taleghani (formerly Samsonite CFO, who led that company’s profitability transformation), who joined in February. Dave Bergman stays through 2027 for the handoff.

For FY25 (year ended March 31, 2025) the math worked. Though revenue fell 9.4%, gross margin climbed 180 bps to 47.9%, the second-highest annual print in the company’s history.

But then Q3 FY26 broke the story. Revenue fell another 5.2%, and this time gross margin fell 310 bps with it to 44.4%, the lowest quarterly print in two years. Tariffs took 200 bps, North America discounting took the rest. The thesis only works if margins hold.

So heading into tomorrow, here’s what we’re watching:

Gross Margin. Full-year FY26 guidance is for gross margin to decline ~190 bps, which after a 9-month YTD of 46.6% implies Q4 lands around 44%. The Street already expects Q3 wasn’t a one-quarter blip. If management frames Q3 as a tariff-driven trough with margin re-accelerating from here, the premium reset thesis may still have life. If they recalibrate the long-term margin algorithm down, “premium reset” will start to look like “managed decline”

North America. Plank narrowed his strategic focus to NA in the FY25 10-K. Q3 NA fell 10.3% to $757 M. Full-year guidance now calls for NA to be down ~8%, which means Q4 needs to be down mid-to-high singles to make the math work. The real read, though, is wholesale-vs-DTC mix: in Q3, wholesale shrank faster (-6.4%) than DTC (-3.9%), with DTC e-commerce down 7% but DTC stores only down 2%. That means full-price store traffic was holding up better than discount-driven channels. If Q4 keeps that pattern, the brand-elevation thesis has legs. Instead, if wholesale stabilizes while DTC accelerates downward, then the consumer is voting against full-price product.

International. EMEA in Q3 was $316M, up 6%, with EMEA operating income up 17% to $49 M. Latin America revenue was up nearly 20%, though LATAM operating income actually fell 44% in the quarter on higher product input costs, marketing, and bad debt expense. This means the LATAM growth comes at a temporary cost. EMEA is now guided to ~9% growth for the year, and APAC’s full-year decline guide just improved from high-singles to ~6%. There’s a real business here that doesn’t show up in the North America narrative, and the long-run mix shift toward international changes the comp set entirely. On Holding, Hoka, and Asics all trade at premium multiples on international-heavy mixes. UA still trades like a struggling US wholesale brand.

The restructuring math. Plank’s 2025 Restructuring Plan started at $70-90M in May 2024, was raised to $140-160M that September, then raised to $255M on November 13, 2025. The last increase included separating the Curry Brand ($69.7M of non-cash contract termination cost in Q3 alone). $224M of the $255M has been incurred through Q3; the rest is supposed to land in Q4. The questions tomorrow: is it actually done? And does management finally quantify the run-rate savings the restructuring is supposed to generate?

Marketing spend. Q3 marketing spend was down 12.6% YoY, and it’s running at 10.5% of revenue versus 11.4% a year ago. Plank is pulling marketing dollars while pulling revenue dollars. The bullish read is that brand health is strong enough to coast, and Plank told the Q2 call that brand awareness among 18-34 year-olds went from “the mid-sixties just six months ago to over eighty percent today,” crediting the “We Are Football” campaign. The bearish read is they’re protecting EBIT because the business can’t absorb restructuring charges AND maintained brand investment. We’ll look to tomorrow’s FY27 marketing posture will tell us which it is.

The single most important sentence in the call will be whatever management says about the FY27 gross margin trajectory and the FY27 EPS number. UBS's Jay Sole expects guidance of $0.25-$0.30 per share with the high end implying low-single-digit revenue growth. If they signal margin reaccelerates and EPS lands in that range or better, the reset thesis is intact and Fairfax's 22% bet starts looking smart. But if they don't, one might read performance as Plank spending eighteen months selling a managed decline.

| A guest post by

|